How Perverted Incentives Caused the Financial Crisis

Executive Summary

Beginning in the mid-1990s, home prices in many American cities began a decade-long climb that proved to be an irresistible opportunity for investors. Along the way, a lot of people made a great deal of money. But by the end of the first decade of the twenty-first century, too many of these investments turned out to be much riskier than many people had thought. Homeowners lost their houses, financial institutions imploded, and the entire financial system was in turmoil.

How did this happen? Whose fault was it? Some blame capitalism for being inherently unstable. Some blame Wall Street for its greed, hubris, and stupidity. But greed, hubris, and stupidity are always with us. What changed in recent years that created such a destructive set of decisions that culminated in the collapse of the housing market and the financial system?

In this paper, I argue that public-policy decisions have perverted the incentives that naturally create stability in financial markets and the market for housing. Over the last three decades, government policy has coddled creditors, reducing the risk they face from financing bad investments. Not surprisingly, this encouraged risky investments financed by borrowed money. The increasing use of debt mixed with housing policy, monetary policy, and tax policy crippled the housing market and the financial sector. Wall Street is not blameless in this debacle. It lobbied for the policy decisions that created the mess.

In the United States we like to believe we are a capitalist society based on individual responsibility. But we are what we do. Not what we say we are. Not what we wish to be. But what we do. And what we do in the United States is make it easy to gamble with other people’s money—particularly borrowed money—by making sure that almost everybody who makes bad loans gets his money back anyway. The financial crisis of 2008 was a natural result of these perverse incentives. We must return to the natural incentives of profit and loss if we want to prevent future crises.

My understanding of the issues in this paper was greatly enhanced and influenced by numerous conversations with Sam Eddins, Dino Falaschetti, Arnold Kling, and Paul Romer. I am grateful to them for their time and patience. I also wish to thank Mark Adelson, Karl Case, Guy Cecala, William Cohan, Stephan Cost, Amy Fontinelle, Zev Fredman, Paul Glashofer, David Gould, Daniel Gressel, Heather Hambleton, Avi Hofman, Brian Hooks, Michael Jamroz, James Kennedy, Robert McDonald, Forrest Pafenberg, Ed Pinto, Rob Raffety, Daniel Rebibo, Gary Stern, John Taylor, Jeffrey Weiss, and Jennifer Zambone for their comments and helpful conversations on various aspects of financial and monetary policy. I received helpful feedback from presentations to the Hoover Institution’s Working Group on Global Markets, George Mason University’s Department of Economics, and the Mercatus Center’s Financial Markets Working Group. I am grateful for research assistance from Benjamin Klutsey and Ryan Langrill. None of the above bears any responsibility for any errors in this paper. In writing this paper, I’ve learned a little too much about how our financial system works. Unfortunately, I’m sure I still have much to learn. And as more of the facts come to light about the behavior of key players in the crisis, I’ll be commenting at my blog, Cafe Hayek, under the category “Gambling with Other People’s Money.”

CONTENTS

2. Gambling with Other People’s Money

3. Did Creditors Expect to Get Rescued?

5. Heads—They Win a Ridiculously Enormous Amount. Tails—They Win Just an Enormous Amount

6. How Creditor Rescue and Housing Policy Combined with Regulation to Blow Up the Housing Market

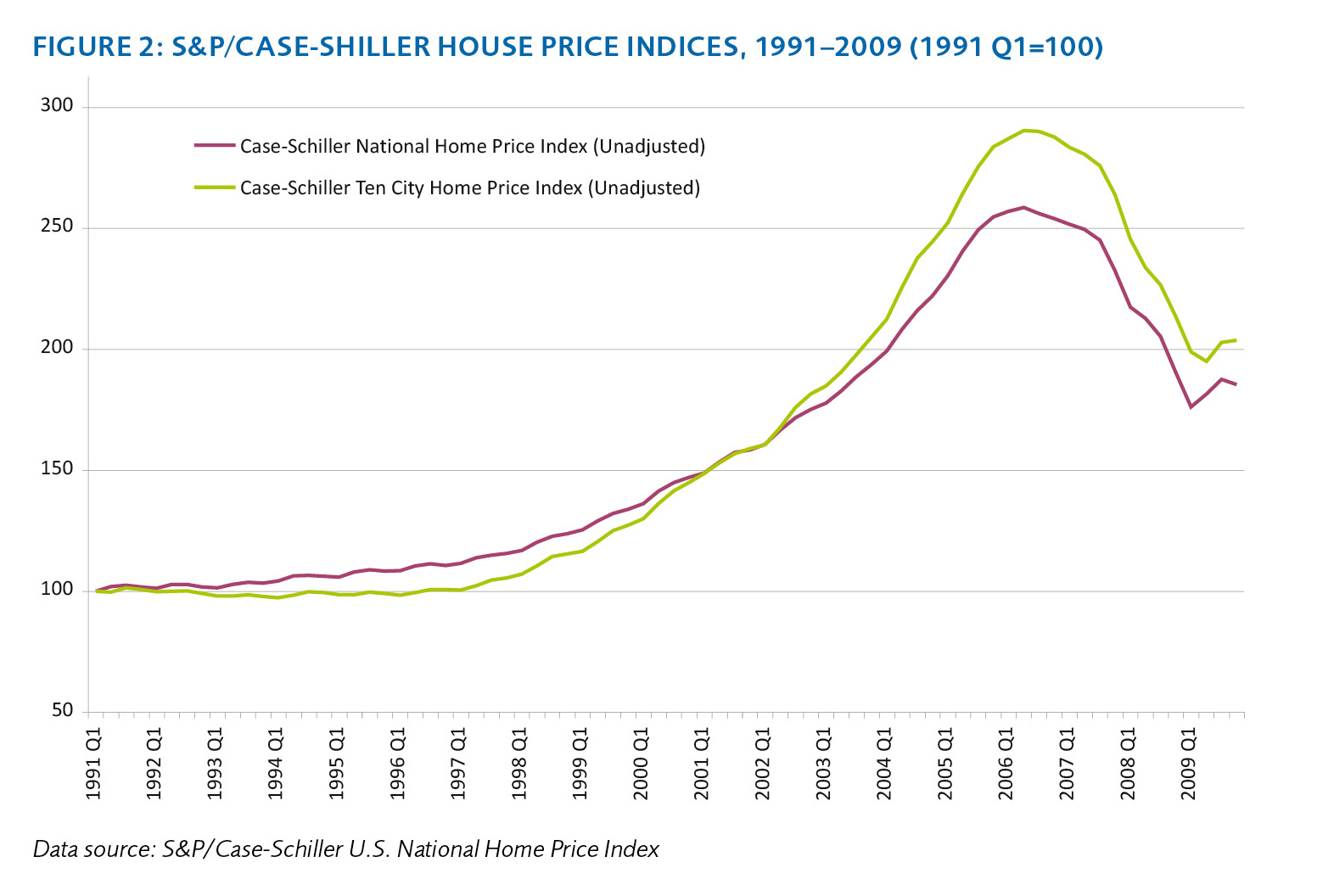

Figure 2: S&P/Case-Shiller House Price Indices, 1991–2009 (1991 Q1=100)

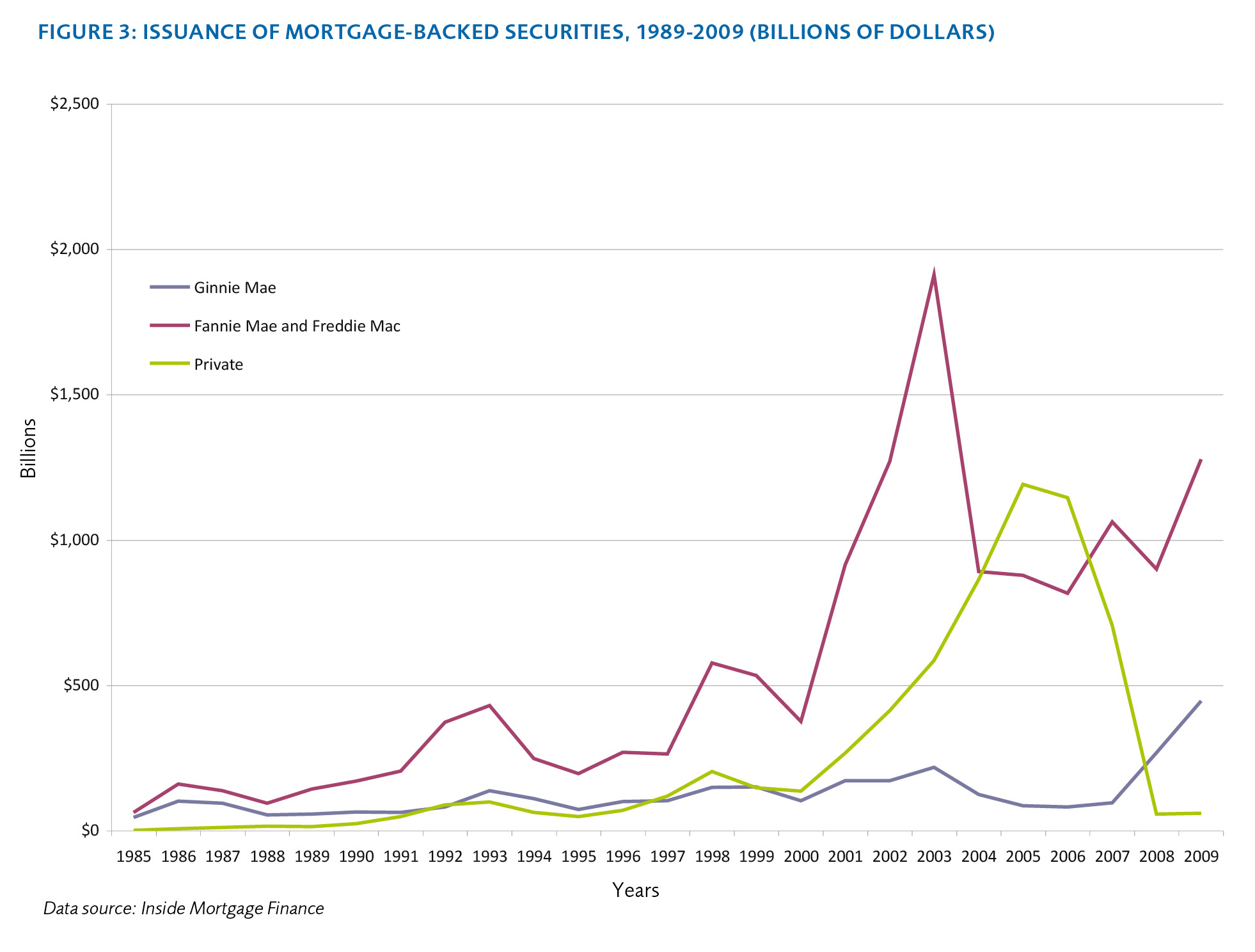

Figure 3: Issuance of Mortgage-Backed Securities, 1989–2009 (Billions of Dollars)

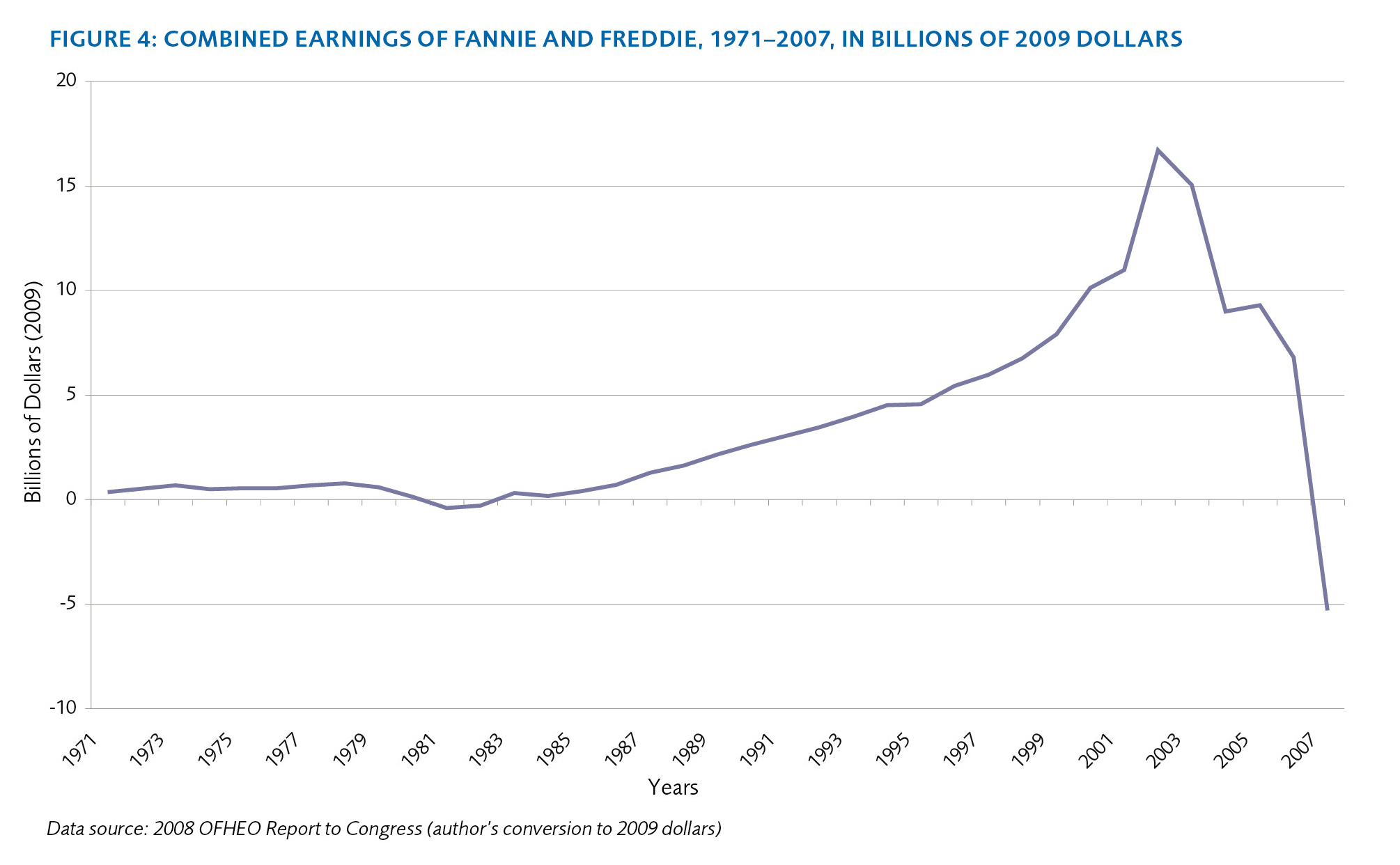

Figure 4: Combined Earnings of Fannie and Freddie, 1971–2007 (Billions of 2009 Dollars)

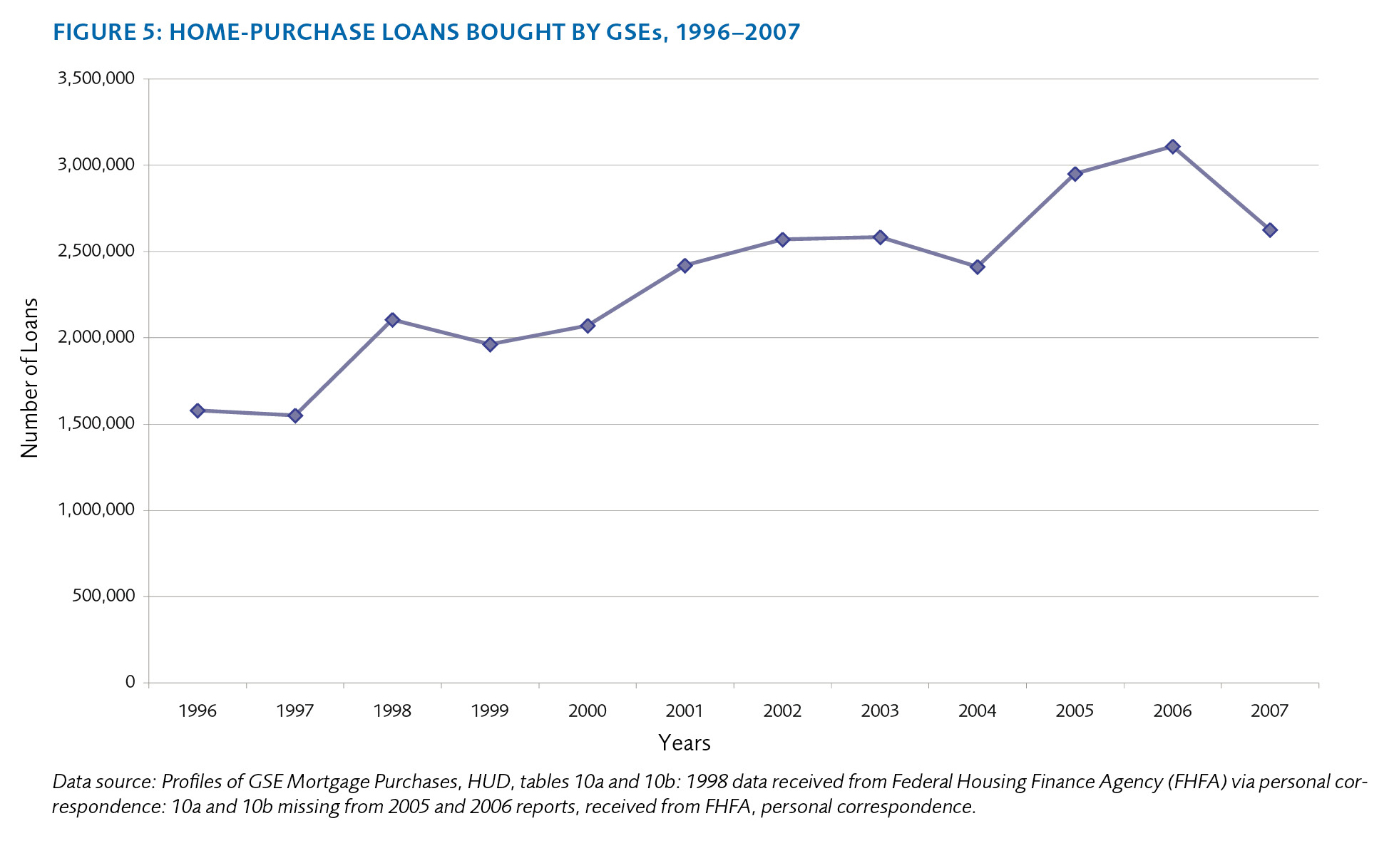

Figure 5: Home-Purchase Loans Bought by GSEs, 1996–2007

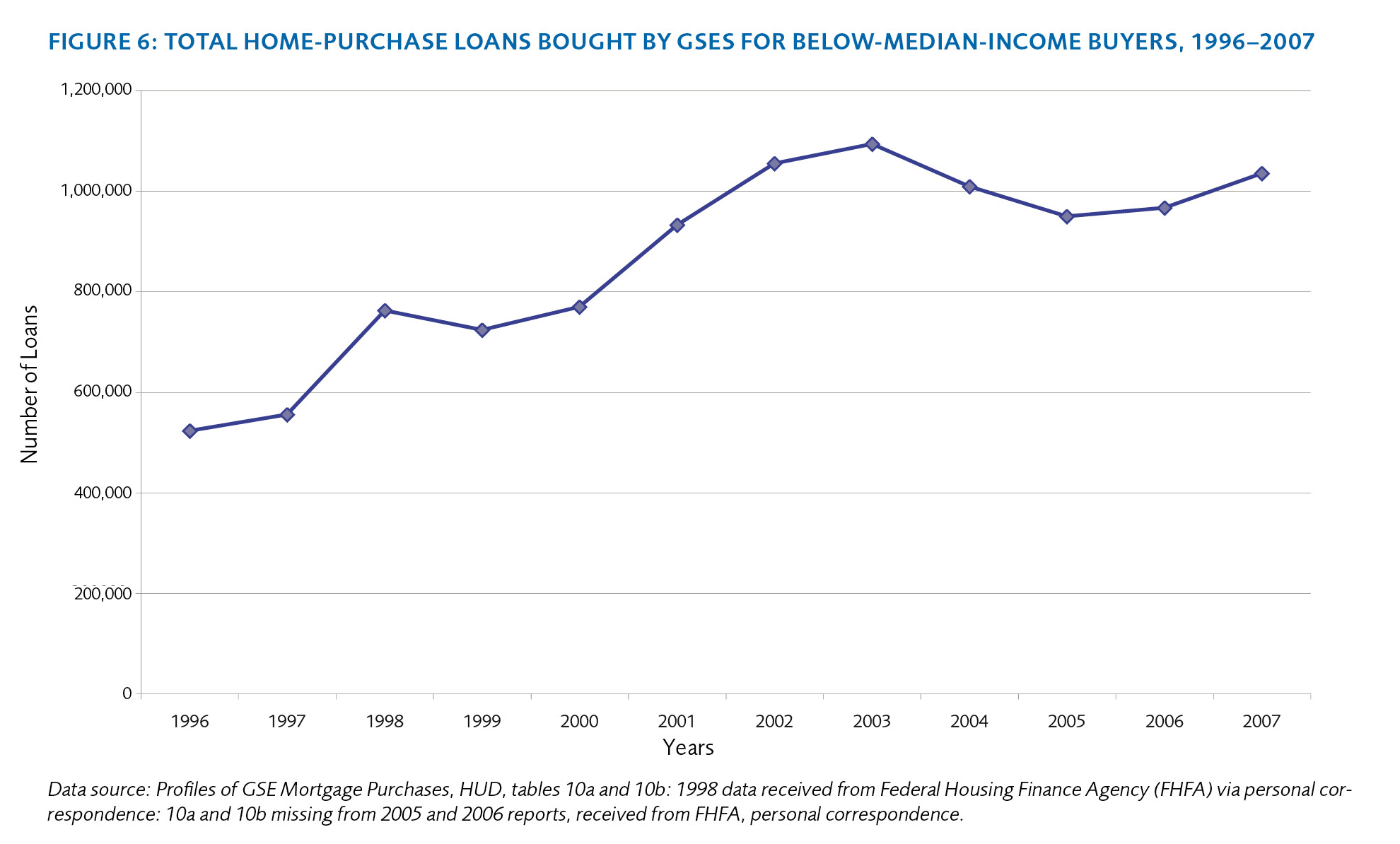

Figure 6: Total Home-Purchase Loans Bought by GSEs for Below-Median-Income Buyers, 1996–2007

Figure 7: Total Home-Purchase Loans Bought by GSEs with Greater than 95% Loan-to-Value Ratios

7B. What Steering the Conduit Really Did

8. Fannie and Freddie—Cause or Effect?

9. Commercial and Investment Banks

Figure 9: Value of Mortgage Originations (Billions of Dollars)

Someday you guys are going to have to tell me how we ended up with a system like this. I know this is not the time to test them and put them through failure, but we’re not doing something right if we’re stuck with these miserable choices.

—President George W. Bush, talking to Ben Bernanke and Henry Paulson when told it was necessary to bail out AIG 1

The curious task of economics is to demonstrate to men how little they really know about what they imagine they can design.

—F. A. Hayek2

1. INTRODUCTION

Beginning in the mid-1990s, home prices in many American cities began a decade-long climb that proved to be an irresistible opportunity for investors.

Along the way, a lot of people made a great deal of money. But by the end of the first decade of the twenty-first century, too many of these investments turned out to be much riskier than many people had thought. Homeowners lost their houses, financial institutions imploded, and the entire financial system was in turmoil.3

How did this happen? Whose fault was it?

A 2009 study by the U.S. Congressional Research Service identified 26 causes of the crisis.4 The Financial Crisis Inquiry Commission is studying 22 different potential causes of the crisis.5 In the face of such complexity, it is tempting to view the housing crisis and subsequent financial crisis as a once-in-a-century coincidental conjunction of destructive forces. As Alan Schwartz, Bear Stearns’s last CEO, put it, “We all [messed] up. Government. Rating agencies. Wall Street. Commercial banks. Regulators. Investors. Everybody.”6

In this commonly held view, the housing market collapse and the subsequent financial crisis were a perfect storm of private and public mistakes. People bought houses they couldn’t afford. Firms bundled the mortgages for these houses into complex securities. Investors and financial institutions bought these securities thinking they were less risky than they actually were. Regulators who might have prevented the mess were asleep on the job. Greed and hubris ran amok. Capitalism ran amok.

To those who accept this narrative, the lesson is clear. As Paul Samuelson put it,

And today we see how utterly mistaken was the Milton Friedman notion that a market system can regulate itself. We see how silly the Ronald Reagan slogan was that government is the problem, not the solution. This prevailing ideology of the last few decades has now been reversed. Everyone understands now, on the contrary, that there can be no solution without government.7

The implication is that we need to reject unfettered capitalism and embrace regulation. But Wall Street and the housing market were hardly unfettered. Yes, deregulation and misregulation contributed to the crisis, but mainly because public policy over the last three decades has distorted the natural feedback loops of profit and loss. As Milton Friedman liked to point out, capitalism is a profit and loss system. The profits encourage risk taking. The losses encourage prudence. When taxpayers absorb the losses, the distorted result is reckless and imprudent risk taking.

A different mistake is to hold Wall Street and the financial sector blameless, for after all, investment bankers and other financial players were just doing what they were supposed to do—maximizing profits and responding to the incentives and the rules of the game. But Wall Street helps write the rules of the game. Wall Street staffs the Treasury Department. Washington staffs Fannie Mae and Freddie Mac. In the week before the AIG bailout that put $14.9 billion into the coffers of Goldman Sachs, Treasury Secretary and former Goldman Sachs CEO Henry Paulson called Goldman Sachs CEO Lloyd Blankfein at least 24 times.8 I don’t think they were talking about how their kids were doing.

This paper explores how changes in the rules of the game—some made for purely financial motives, some made for more altruistic reasons—created the mess we are in.

The most culpable policy has been the systematic encouragement of imprudent borrowing and lending. That encouragement came not from capitalism or markets, but from crony capitalism, the mutual aid society where Washington takes care of Wall Street and Wall Street returns the favor.9 Over the last three decades, public policy has systematically reduced the risk of making bad loans to risky investors. Over the last three decades, when large financial institutions have gotten into trouble, the government has almost always rescued their bondholders and creditors. These policies have created incentives both to borrow and to lend recklessly.

When large financial institutions get in trouble, equity holders are typically wiped out or made to suffer significant losses when share values plummet. The punishment of equity holders is usually thought to reduce the moral hazard created by the rescue of creditors. But it does not. It merely masks the role of creditor rescues in creating perverse incentives for risk taking.

The expectation by creditors that they might be rescued allows financial institutions to substitute borrowed money for their own capital even as they make riskier and riskier investments. Because of the large amounts of leverage—the use of debt rather than equity—executives can more easily generate short-term profits that justify large compensation. While executives endure some of the pain if short-term gains become losses in the long run, the downside risk to the decision-makers turns out to be surprisingly small, while the upside gains can be enormous. Taxpayers ultimately bear much of the downside risk. Until we recognize the pernicious incentives created by the persistent rescue of creditors, no regulatory reform is likely to succeed.

Almost all of the lenders who financed bad bets in the housing market paid little or no cost for their recklessness. Their expectations of rescue were confirmed. But the expectation of creditor rescue was not the only factor in the crisis. As I will show, housing policy, tax policy, and monetary policy all contributed, particularly in their interaction. Though other factors—the repeal of the Glass-Steagall Act, predatory lending, fraud, changes in capital requirements, and so on—made things worse, I focus on creditor rescue, housing policy, tax policy, and monetary policy because without these policies and their interaction, the crisis would not have occurred at all. And among causes, I focus on creditor rescue and housing policy because they are the most misunderstood.

In the United States we like to believe we are a capitalist society based on individual responsibility. But we are what we do. Not what we say we are. Not what we wish to be. But what we do. And what we do is make it easy to gamble with other people’s money—particularly borrowed money—by making sure that almost everybody who makes bad loans gets his money back anyway. The financial crisis of 2008 was a natural result of these perverse incentives.

2. GAMBLING WITH OTHER PEOPLE’S MONEY

Imagine a superb poker player who asks you for a loan to finance his nightly poker playing.10 For every $100 he gambles, he’s willing to put up $3 of his own money. He wants you to lend him the rest. You will not get a stake in his winning. Instead, he’ll give you a fixed rate of interest on your $97 loan.

The poker player likes this situation for two reasons. First, it minimizes his downside risk. He can only lose $3. Second, borrowing has a great effect on his investment—it gets leveraged. If his $100 bet ends up yielding $103, he has made a lot more than 3 percent—in fact, he has doubled his money. His $3 investment is now worth $6.

But why would you, the lender, play this game? It’s a pretty risky game for you. Suppose your friend starts out with a stake of $10,000 for the night, putting up $300 himself and borrowing $9,700 from you. If he loses anything more than 3 percent on the night, he can’t make good on your loan.

Not to worry—your friend is an extremely skilled and prudent poker player who knows when to hold ,em and when to fold ,em. He may lose a hand or two because poker is a game of chance, but by the end of the night, he’s always ahead. He always makes good on his debts to you. He has never had a losing evening. As a creditor of the poker player, this is all you care about. As long as he can make good on his debt, you’re fine. You care only about one thing—that he stays solvent so that he can repay his loan and you get your money back.

But the gambler cares about two things. Sure, he too wants to stay solvent. Insolvency wipes out his investment, which is always unpleasant—it’s bad for his reputation and hurts his chances of being able to use leverage in the future. But the gambler doesn’t just care about avoiding the downside. He also cares about the upside. As the lender, you don’t share in the upside; no matter how much money the gambler makes on his bets, you just get your promised amount of interest.

If there is a chance to win a lot of money, the gambler is willing to a take a big risk. After all, his downside is small. He only has $3 at stake. To gain a really large pot of money, the gambler will take a chance on an inside straight.

As the lender of the bulk of his funds, you wouldn’t want the gambler to take that chance. You know that when the leverage ratio—the ratio of borrowed funds to personal assets—is 32–1 ($9700 divided by $300), the gambler will take a lot more risk than you’d like. So you keep an eye on the gambler to make sure that he continues to be successful in his play.

But suppose the gambler becomes increasingly reckless. He begins to draw to an inside straight from time to time and pursue other high-risk strategies that require making very large bets that threaten his ability to make good on his promises to you. After all, it’s worth it to him. He’s not playing with very much of his own money. He is playing mostly with your money. How will you respond?

You might stop lending altogether, concerned that you will lose both your interest and your principal. Or you might look for ways to protect yourself. You might demand a higher rate of interest. You might ask the player to put up his own assets as collateral in case he is wiped out. You might impose a covenant that legally restricts the gambler’s behavior, barring him from drawing to an inside straight, for example.

These would be the natural responses of lenders and creditors when a borrower takes on increasing amounts of risk. But this poker game isn’t proceeding in a natural state. There’s another person in the room: Uncle Sam. Uncle Sam is off in the corner, keeping an eye on the game, making comments from time to time, and, every once in a while, intervening in the game.

He sets many of the rules that govern the play of the game. And sometimes he makes good on the debt of the players who borrow and go bust, taking care of the lenders. After all, Uncle Sam is loaded. He has access to funds that no one else has. He also likes to earn the affection of people by giving them money. Everyone in the room knows Uncle Sam is loaded, and everyone in the room knows there is a chance, perhaps a very good chance, that wealthy Uncle Sam will cover the debts of players who go broke.

Nothing is certain. But the greater the chance that Uncle Sam will cover the debts of the poker player if he goes bust, the less likely you are to try to restrain your friend’s behavior at the table. Uncle Sam’s interference has changed your incentive to respond when your friend makes riskier and riskier bets.

If you think that Uncle Sam will cover your friend’s debts . . .

you will worry less and pay less attention to the risk-taking behavior of your gambler friend.

you will not take steps to restrain reckless risk taking.

you will keep making loans even as his bets get riskier.

you will require a relatively low rate of interest for your loans.

you will continue to lend even as your gambler friend becomes more leveraged.

you will not require that your friend put in more of his own money and less of yours as he makes riskier and riskier bets.

What will your friend do when you behave this way? He’ll take more risks than he would normally. Why wouldn’t he? He doesn’t have much skin in the game in the first place. You do, but your incentive to protect your money goes down when you have Uncle Sam as a potential backstop.

Capitalism is a profit and loss system. The profits encourage risk taking. The losses encourage prudence. Eliminate losses or even raise the chance that there will be no losses and you get less prudence. So when public decisions reduce losses, it isn’t surprising that people are more reckless.

Who got to play with other people’s money in the years preceding the crisis? Who was highly leveraged—putting very little of his own money at risk while borrowing the rest? Who was able to continue to borrow at low rates even as he made riskier and riskier bets? Who sat at the poker table?

Just about everybody.

Homebuyers. The government-sponsored enterprises (GSEs)—Fannie Mae and Freddie Mac. The commercial banks—Bank of America, Citibank, and many others. The investment banks—like Bear Stearns and Lehman Brothers. Everyone was playing the same game, playing with other people’s money. They were all able to continue borrowing at the same low rates even as the bets they placed grew riskier and riskier. Only at the very end, when collapse was imminent and there was doubt about whether Uncle Sam would really come to the rescue, did the players at the table find it hard to borrow and gamble with other people’s money.

Without extreme leverage, the housing meltdown would have been like the meltdown in high-tech stocks in 2001—a bad set of events in one corner of a very large and diversified economy.11 Firms that invested in that corner would have had a bad quarter or a bad year. But because of the amount of leverage that was used, the firms that invested in housing—Fannie Mae and Freddie Mac, Bear Stearns, Lehman Brothers, Merrill Lynch, and others—destroyed themselves.

So why did it happen? Did bondholders and lenders really believe that they would be rescued if their investments turned out to be worthless? Were the expectations of a bailout sufficiently high to reduce the constraints on leverage? And even though it is pleasant to gamble with other people’s money, wasn’t a lot of that money really their own? Even if bondholders and lenders didn’t restrain the recklessness of those to whom they lent, why didn’t stockholders—who were completely wiped out in almost every case, losing their entire investments—restrain recklessness? Sure, bondholders and lenders care only about avoiding the downside. But stockholders don’t care just about the upside. They don’t want to be wiped out, either. The executives of Fannie Mae, Freddie Mac, and the large investment banks held millions, sometimes hundreds of millions of their own wealth in equity in their firms. They didn’t want to go broke and lose all that money. Shouldn’t that have restrained the riskiness of the bets that these firms took?

3. DID CREDITORS EXPECT TO GET RESCUED?

Was it reasonable for either investors or their creditors to expect government rescue?12 While there were government bailouts of Lockheed and Chrysler in the 1970s, the recent history of rescuing large, troubled financial institutions begins in 1984, when Continental Illinois, then one of the top ten banks in the United States, was rescued before it could fail. The story of its collapse sounds all too familiar—investments that Continental Illinois had made with borrowed money turned out to be riskier than the market had anticipated. This caused what was effectively a run on the bank, and Continental Illinois found itself unable to cover its debts with new loans.

In the government rescue, the government took on $4.5 billion of bad loans and received an 80 percent equity share in the bank. Only 10 percent of the bank’s deposits were insured, but every depositor was covered in the rescue.13 Eventually, equity holders were wiped out.

In congressional testimony after the rescue, the comptroller of the currency implied that there were no attractive alternatives to such rescues if the 10 or 11 largest banks in the United States experienced similar problems.14 The rescue of Continental Illinois and the subsequent congressional testimony sent a signal to the poker players and those that lend to them that lenders might be rescued.

Continental Illinois was just the largest and most dramatic example of a bank failure in which creditors were spared any pain. Irvine Sprague, in his 1986 book Bailout noted,

Of the fifty largest bank failures in history, forty-six—including the top twenty—were handled either through a pure bailout or an FDIC assisted transaction where no depositor or creditor, insured or uninsured, lost a penny.15

The 50 largest failures up to that time all took place in the 1970s and 1980s. As the savings and loan (S&L) crisis unfolded during the 1980s, government repeatedly sent the same message: lenders and creditors would get all of their money back. Between 1979 and 1989, 1,100 commercial banks failed. Out of all of their deposits, 99.7 percent, insured or uninsured, were reimbursed by policy decisions.16

The next event that provided information to the poker players was the collapse of Drexel Burnham in 1990.17 Drexel Burnham lobbied the government for a guarantee of its bad assets that would allow a suitor to find the company attractive. But Drexel went bankrupt with no direct help from the government. The failure to rescue Drexel put some threat of loss back into the system, but maybe not very much—Drexel Burnham was a political pariah. The firm and its employees had numerous convictions for securities fraud and other violations.

In 1995 there was another rescue, not of a financial institution, but of a country—Mexico. The United States orchestrated a $50 billion rescue of the Mexican government, but as in the case of Continental Illinois, it was really a rescue of the creditors, those who had bought Mexican bonds and who faced large losses if Mexico were to default. As Charles Parker details in his 2005 study, Wall Street investment banks had strong interests in Mexico’s financial health (because of future underwriting fees) and held significant amounts of Mexican bonds and securities.18 Despite opposition from Main Street and numerous politicians, policy makers put together the rescue in the name of avoiding a financial crisis. Ultimately, the U.S. Treasury got its money back and even made a modest profit, causing some to deem the rescue a success. It was a success in fiscal terms. But it encouraged lenders to finance risky bets without fear of the consequences.

Willem Buiter, then an economics professor at the University of Cambridge and now the chief economist at CitiGroup, was quoted at the time saying:

This is not a great incentive for efficient operations of financial markets, because people do not have to weigh carefully risk against return. They’re given a one-way bet, with the U.S. Treasury and the international community underwriting the default risk. That makes for lazy private investors who don’t have to do their homework figuring out what the risks are.19

Or to put it informally, all profit and no loss make Jack a dull boy.

The next major relevant event on Wall Street was the 1998 collapse of Long-Term Capital Management (LTCM), a highly leveraged private hedge fund.20 When its investments soured, its access to liquidity dried up and it faced insolvency. There was a fear that the death of LTCM would take down many of its creditors.

The president of the Federal Reserve Bank of New York, William McDonough, convened a meeting of the major creditors—Bankers Trust, Barclays, Bear Stearns, Chase Manhattan, Credit Suisse, First Boston, Deutsche Bank, Goldman Sachs, J. P. Morgan, Lehman Brothers, Merrill Lynch, Morgan Stanley, Parabas, Salomon Smith Barney, Société Générale, and UBS. The meeting was “voluntary” as was ultimately the participation in the rescue that the Fed orchestrated.

Most of the creditors agreed to put up $300 million apiece. Lehman Brothers put up $100 million. Bear Stearns contributed nothing. All together, they raised $3.625 billion. In return, the creditors received 90 percent of the firm. Ultimately, LTCM died. While creditors were damaged, the losses were much smaller than they would have been in a bankruptcy. No government money was involved. Yet the rescue of LTCM did send a signal that the government would try to prevent bankruptcy and creditor losses.

In addition to all of these public and dramatic interventions by the Fed and the Treasury, there were many examples of regulatory forbearance—where government regulators suspended compliance with capital requirements. There were also the seemingly systematic efforts by the Federal Reserve beginning in 1987 and continuing throughout the Greenspan and Bernanke eras to use monetary policy to keep asset prices (equities and housing in particular) bubbling along.21 All of these actions reduced investors’ and creditors’ worries of losses.22

That brings us to the current mess that began in March 2008. There is seemingly little rhyme or reason to the pattern of government intervention. The government played matchmaker and helped Bear Stearns get married to J. P. Morgan Chase. The government essentially nationalized Fannie and Freddie, placing them into conservatorship, honoring their debts, and funding their ongoing operations through the Federal Reserve. The government bought a large stake in AIG and honored all of its obligations at 100 cents on the dollar. The government funneled money to many commercial banks.

Each case seems different. But there is a pattern. Each time, the stockholders in these firms are either wiped out or see their investments reduced to a trivial fraction of what they were before. The bondholders and lenders are left untouched. In every case other than that of Lehman Brothers, bondholders and lenders received everything they were promised: 100 cents on the dollar. Many of the poker players—and almost all of those who financed the poker players—lived to fight another day. It’s the same story as Continental Illinois, Mexico, and LTCM—a complete rescue of creditors and lenders.

The only exception to the rescue pattern was Lehman. Its creditors had to go through the uncertainty, delay, and the likely losses of bankruptcy. The balance sheet at Lehman looked a lot like the balance sheet at Bear Stearns—lots of subprime securities and lots of leverage. What should executives at Lehman have done in the wake of Bear Stearns’ collapse? What would you do if you were part of the executive team at Lehman and you had seen your storied competitor disappear? The death of Bear Stearns should have been a wake-up call. But the rescue of Bear’s creditors let Lehman keep playing the same game as before.

If Bear had been left to die, there would have been pressure on Lehman to raise capital, get rid of the junk on its balance sheet, and clean up its act. There were a variety of problems with this strategy: Lehman might have found it hard to raise capital. It might have found that the junk on its balance sheet was worth very little, and it might not have been worth it for the company to clean up its act. What Lehman actually did though is unclear. It appears to have raised some extra cash and sold off some assets. But it remained highly leveraged, still at least 25–1 in the summer of 2008.23 How did it keep borrowing at all given the collapse of Bear Stearns?

One of Lehman’s lenders was the Reserve Primary money market fund. It held $785 million of Lehman Brothers commercial paper when Lehman collapsed. When Lehman entered bankruptcy, those holdings were deemed to be worthless, and Reserve Primary broke the buck, lowering its net asset value to 97 cents. Money market funds are considered extremely safe investments in that their net asset value normally remains constant at $1, but on that day, Reserve Primary’s fund holders suffered a capital loss. What was a money market fund doing investing in Lehman Brothers debt in the aftermath of the Bear Stearns debacle? Didn’t Reserve’s executives know Lehman’s balance sheet looked a lot like Bear’s? Surely they did. Presumably they assumed that the government would treat Lehman like it treated Bear. It seems they expected a rescue in the worst-case scenario.

They weren’t alone. When Bear collapsed, Lehman’s credit default swaps spiked, but then fell steadily after Bear’s creditors were rescued through mid-May (see figure 1), even as the price of Lehman’s stock fell steadily after January.24 This suggests that investors expected Lehman to be rescued as Bear was in the case of a Lehman collapse.25 Many economists have blamed the government’s failure to rescue Lehman as the cause of the panic that ensued.26 But why would Lehman’s failure cause a panic? What was the new information that investors reacted to? After the failure of Bear Stearns, many speculated that Lehman was next. It was well known that Lehman’s balance sheet was highly leveraged with assets similar to Bear’s.27 The government’s refusal to rescue Lehman, or at least its creditors, caused the financial market to shudder, not because of any direct consequences of a Lehman bankruptcy but because it signaled that the implicit policy of rescuing creditors might not continue.

View Figure 1, “Guarded: The annual coast to buy protection against default on $10 million of Lehman debt for five years,” at WSJ.com.

The new information in the Lehman collapse was that future creditors might indeed be at risk and that the party might be over. That conclusion was quickly reversed with the rescue of AIG and others. But it sure sobered up the drinkers for a while.

Did this history of government rescuing creditors and lenders encourage the recklessness of the lenders who financed the bad bets that led to the financial crisis of 2008?

For the GSEs’ creditors, the answer is almost certainly yes. Fannie Mae and Freddie Mac’s counterparties expected the U.S. government to stand behind Fannie and Freddie, which of course it ultimately did. This belief allowed Fannie and Freddie to borrow at rates near those of the Treasury.

From January 2000 through mid-2003, the spreads of Fannie Mae and Freddie Mac bonds versus Treasuries—the rate at which Fannie and Freddie could borrow money compared to the United States government—were low and falling. Those spreads stayed low and steady through early 2007. Between 2000 and Fall 2008 when Fannie and Freddie were essentially nationalized, the rate on Fannie and Freddie’s five-year debt over and above Treasuries was almost always less than 1 percent. From 2003 through 2006 it was about a third of a percentage point.28 Yet between 2000 and 2007, as I show below, Fannie and Freddie were acquiring riskier and riskier loans which ultimately led to their death. Why didn’t lenders to Fannie and Freddie require a bigger premium as Fannie and Freddie took on more risk?

The answer is that they saw lending to the GSEs as no riskier than lending money to the U.S. government. Not quite the same, of course. GSEs do not have quite the same credit risk as the U.S. government. There was a chance that the government would let Fannie or Freddie go bankrupt. That’s why the premium rose in 2007, but even then, it was still under 1 percent through September 2008.29

The unprecedented expansion of Fannie and Freddie’s activities even as their portfolio became more risky helped create the housing bubble. That eventually led to their demise and conservatorship, the polite name for what is really nationalization. The government has already paid out over $100 billion dollars on Fannie and Freddie’s behalf, with a much higher bill likely to come in the future.30

But, what about the lenders to the commercial banks and the investment banks? Yes, the government bailed out all the lenders other than those that lent to Lehman. Yes, many institutions that had made bad bets survived instead of going bankrupt. But did this reality and all the rescues of the 1980s and 1990s really affect the behavior of lenders in advance of the rescues?

We can’t know with certainty. No banker will step forward and say that past bailouts and the “Greenspan put” caused him to be less prudent and made him feel good about lending money to Bear Stearns. No executive at Bear Stearns will say that he reassured nervous lenders by telling them that the government would step in. And Goldman Sachs continues to claim that it is part of a “virtuous cycle” of raising capital and creating wealth and jobs, that it converted into a bank holding company to “restore confidence in the financial system as a whole,” and that the rescue of AIG had no effect on its bottom line.31 (Right. And I’m going to be the starting point guard for the Boston Celtics next year.)

While direct evidence is unlikely, the indirect evidence relies on how people generally behave in situations of uncertainty. When expected costs are lowered, people behave more recklessly. When football players make a tackle, they don’t consciously think about the helmet protecting them, but safer football equipment encourages more violence on the field. Few people think that it’s okay to drive faster on a rainy night when they have seatbelts, airbags, and antilock brakes, but that is how they behave.32 Not all motivations are direct and conscious.33

There is even some evidence of conscious expectations of rescue, though it is necessarily anecdotal. Andrew Haldane, the Executive Director of Financial Stability of the Bank of England, tells this story about the stress-testing simulations that banks conduct— examining worst-case scenarios for interest rates, the state of the economy, and so on—to make sure they have enough capital to survive:

A few years ago, ahead of the present crisis, the Bank of England and the FSA [Financial Services Authority] commenced a series of seminars with financial firms, exploring their stress-testing practices. The first meeting of that group sticks in my mind. We had asked firms to tell us the sorts of stress which they routinely used for their stress-tests. A quick survey suggested these were very modest stresses. We asked why. Perhaps disaster myopia—disappointing, but perhaps unsurprising? Or network externalities—we understood how difficult these were to capture?

No. There was a much simpler explanation according to one of those present. There was absolutely no incentive for individuals or teams to run severe stress tests and show these to management. First, because if there were such a severe shock, they would very likely lose their bonus and possibly their jobs. Second, because in that event the authorities would have to step-in anyway to save a bank and others suffering a similar plight.

All of the other assembled bankers began subjecting their shoes to intense scrutiny. The unspoken words had been spoken. The officials in the room were aghast. Did banks not understand that the official sector would not underwrite banks mis-managing their risks?

Yet history now tells us that the unnamed banker was spot-on. His was a brilliant articulation of the internal and external incentive problem within banks. When the big one came, his bonus went and the government duly rode to the rescue.34

The only difference between this scenario in the United Kingdom and the one in the United States is that in the U.S. the Fed came to the rescue and the executives, for the most part, kept their bonuses.

4. WHAT ABOUT EQUITY HOLDERS?

Creditors do not share in the upside of any investment. So they only care about one thing—avoiding the downside. They want to make sure their counterparty is going to stay solvent. Equity holders care about two things—the upside and the downside. So why doesn’t fear of the downside encourage prudence? Even if creditors were lulled into complacency by the prospects of rescue, shareholders—who are usually wiped out—wouldn’t want too much risk, would they?

Why would Bear Stearns, Lehman Brothers, and Merrill Lynch take on so much risk? They didn’t want to go bankrupt and wipe out the equity holders. Why would these firms leverage themselves 30–1 and 40–1, putting the existence of the firm at risk in the event of a small change in the value of the assets in their portfolios? Surely the equity holders would rebel against such leverage.

But very few equity holders put all their eggs in one basket. Buying risky stocks isn’t just for high fliers looking for high risk and high rewards. It also attracts people who want high risk and high rewards in part of their portfolios. It’s all about risk and return along with diversification. The Fannie Mae stock held in an investor’s portfolio might be high risk and (he hopes) high return. If that makes a Fannie Mae stockholder nervous, he can also buy Fannie Mae bonds. The bonds are low risk, low return. He can even hold a mix of equity and bonds to mimic the overall return to highly leveraged Fannie Mae in its entirety. For every $100 he invests, he buys $97 of Fannie’s bonds and $3 of equity, for example. When the stock is doing well, the equity share boosts the return of the safe bonds. In the worst-case scenario, Fannie Mae goes broke, wiping out the investor’s equity. But in the meanwhile, he made money on the bonds and maybe even on the stocks if he got out in time.

The same is true of investors holding Bear Stearns or Lehman stock. In 2005, Bear Stearns had its own online subprime mortgage lender, BearDirect. Bear Stearns also owned EMC, a subprime mortgage company. Bear was generating subprime loans and bundling them into mortgage-backed securities, making an enormous amount of money as the price of housing continued to rise. All through 2006 and most of 2007, things were better than fine. The price of Bear Stearns’ stock hit $172. If an investor sold then or even a lot later, he did very, very well. Even though he knew there was a risk that the stock could not just go down, but go down a lot, he didn’t want to discourage the risk taking. He wanted to profit from it.

5. HEADS—THEY WIN A RIDICULOUSLY ENORMOUS AMOUNT. TAILS—THEY WIN JUST AN ENORMOUS AMOUNT

But what about the executives of Bear Stearns, Lehman Brothers, or Merrill Lynch? Their investments were much less diversified than those of the equity holders. Year after year, the executives were being paid in cash and stock options until their equity holdings in their own firms become a massive part of their wealth. Wouldn’t that encourage prudence?

Let’s go back to the poker table and consider how the incentives work when the poker player isn’t just risking his own money alongside that of his lenders. He’s also drawing a salary and bonus and stock options while he’s playing. Some of that compensation is a function of the profitability of the company, which appears to align the incentives of the executives with those of other equity holders. But when leverage is so large, the executive can take riskier bets, generating large profits in the short run and justifying a larger salary. The downside risk is cushioned by his ability to accumulate salary and bonuses in advance of failure.

As Lucian Bebchuk and Holger Spamann have shown, the incentives in the banking business are such that the expected returns to bank executives from bad investments can be quite large even when the effects on the firm are quite harmful. The upside is unlimited for the executives while the downside is truncated:

Because top bank executives were paid with shares of a bank holding company or options on such shares, and both banks and bank holding companies obtained capital from debt-holders, executives faced asymmetric payoffs, expecting to benefit more from large gains than to lose from large losses of a similar magnitude . . .

Our basic argument can be seen in a simple example. A bank has $100 of assets financed by $90 of deposits and $10 of capital, of which $4 are debt and $6 are equity; the bank’s equity is in turn held by a bank holding company, which is financed by $2 of debt and $4 of equity and has no other assets; and the bank manager is compensated with some shares in the bank holding company. On the downside, limited liability protects the manager from the consequences of any losses beyond $4. By contrast, the benefits to the manager from gains on the upside are unlimited. If the manager does not own stock in the holding company but rather options on its stock, the incentives are even more skewed. For example, if the exercise price of the option is equal to the current stock price, and the manager makes a negative-expected-value bet, the manager may have a great deal to gain if the bet turns out well and little to lose if the bet turns out poorly.35

George Akerlof and Paul Romer describe similar incentives in the context of the S&L collapse.36 In Looting: The Economic Underworld of Bankruptcy for Profit, they describe how the owners of S&Ls would book accounting profits, justifying a large salary even though those profits had little or no chance of becoming real. They would generate cash flow by offering an attractive rate on the savings accounts they offered. Depositors would not worry about the viability of the banks because of FDIC insurance. But the owners’ salaries were ultimately coming out of the pockets of taxpayers. What the owners were doing was borrowing money to finance their salaries, money that the taxpayers guaranteed. When the S&Ls failed, the depositors got their money back, and the owners had their salaries: The taxpayers were the only losers.

This kind of looting and corruption of incentives is only possible when you can borrow to finance highly leveraged positions. This in turn is only possible if lenders and bondholders are fools—or if they are very smart and are willing to finance highly leveraged bets because they anticipate government rescue.

In the current crisis, commercial banks, investment banks, and Fannie and Freddie generated large short-term profits using extreme leverage. These short-term profits alongside rapid growth justified enormous salaries until the collapse came. Who lost when this game collapsed? In almost all cases, the lenders who financed the growth avoided the costs. The taxpayers got stuck with the bill, just as they did in the S&L crisis. Ultimately, the gamblers were playing with other people’s money and not their own.

But didn’t executives lose a great deal of money when their companies collapsed? Why didn’t fear of that outcome deter their excessive risk taking? After all, Jimmy Cayne, the CEO of Bear Stearns, and Richard Fuld, the CEO of Lehman Brothers, each lost over a billion dollars when their stock holdings were virtually wiped out. Cayne ended up selling his 6 million shares of Bear Stearns for just over $10 per share. Fuld ended up selling millions of shares for pennies per share.

Surely they didn’t want this to happen.

They certainly didn’t intend for it to happen. This was a game of risk and reward, and in this round, the cards didn’t come through. That was a gamble the executives had been willing to take in light of the huge rewards they had already earned and the even larger rewards they would have pocketed if the gamble had gone well. They saw it as a risk well worth taking.

After all, their personal downsides weren’t anything close to zero. Here is Cayne’s assessment of the outcome:

The only people [who] are going to suffer are my heirs, not me. Because when you have a billion six and you lose a billion, you’re not exactly like crippled, right?37

The worst that could happen to Cayne in the collapse of Bear Stearns, his downside risk, was a stock wipeout, which would leave him with a mere half a billion dollars gained from his prudent selling of shares of Bear Stearns and the judicious investment of the cash part of his compensation.38 Not surprisingly, Cayne didn’t put all his eggs in one basket. He left himself a healthy nest egg outside of Bear Stearns.

Fuld did the same thing. He lost a billion dollars of paper wealth, but he retained over $500 million, the value of the Lehman stock he sold between 2003 and 2008. Like Cayne, he surely would have preferred to be worth $1.5 billion instead of a mere half a billion, but his downside risk was still small.

When we look at Cayne and Fuld, it is easy to focus on the lost billions and overlook the hundreds of millions they kept. It is also easy to forget that the outcome was not preordained. They didn’t plan on destroying their firms. They didn’t intend to. They took a chance. Maybe housing prices plateau instead of plummet. Then you get your $1.5 billion. It was a roll of the dice. They lost.

When Cayne and Fuld were playing with other people’s money, they doubled down, the ultimate gamblers. When they were playing with their own money, they were prudent. They acted like bankers. (Or the way bankers once acted when their own money or the money of their partnership was at stake.39) They held significant amounts of personal funds outside of their own companies’ stock, making their downside risks much smaller than they appeared. They each had a big cushion to land on when their companies went over the cliff. Those cushions were made from other people’s money, the money that was borrowed, the money that let them make high rates of return while the good times rolled and justified their big compensation packages until things fell apart.

What about the executives of other companies? Cayne and Fuld weren’t alone. Angelo Mozillo, the CEO of Countrywide, realized over $400 million in compensation between 2003 and 2008.40 Numerous executives made over $100 million in compensation during the same period.41 Bebchuk, Cohen, and Spamann have looked at the sum of cash bonuses and stock sales by the CEOs and the next four executives at Bear Stearns and Lehman Brothers between 2000 and 2008. It’s a very depressing spectacle. The top five Bear Stearns executives managed to score $1.5 billion during that period. The top five executives at Lehman Brothers had to settle for $1 billion.42 Nice work if you can get it.

The standard explanations for the meltdown on Wall Street are that executives were overconfident. Or they believed their models that assumed Gaussian distributions of risk when the distributions actually had fat tails. Or they believed the ratings agencies. Or they believed that housing prices couldn’t fall. Or they believed some permutation of these many explanations.

These explanations all have some truth in them. But the undeniable fact is that these allegedly myopic and overconfident people didn’t endure any economic hardship because of their decisions. The executives never paid the price. Market forces didn’t punish them, because the expectation of future rescue inhibited market forces. The “loser” lenders became fabulously rich by having enormous amounts of leverage, leverage often provided by another lender, implicitly backed with taxpayer money that did in fact ultimately take care of the lenders.

And many gamblers won. Lloyd Blankfein, the CEO of Goldman Sachs, Jamie Dimon, the CEO of J. P. Morgan Chase, and the others played the same game as Cayne and Fuld. Goldman and J. P. Morgan invested in subprime mortgages. They were highly leveraged. They didn’t have as much toxic waste on their balance sheets as some of their competitors. They didn’t have quite as much leverage, but they were still close to the edge. They were playing a very high-stakes game, with high risk and potential reward. And they survived. Blankfein’s stock in Goldman Sachs is worth over $500 million, and like Cayne and Fuld, he surely has a few assets elsewhere. Like Cayne and Fuld, Blankfein took tremendous risk with the prospect of high reward. His high monetary reward came through, as did his intangible reward in the perpetual poker game of ego. Unlike Cayne and Fuld, Blankfein and Dimon get to hold their heads extra high at the cocktail parties, political fundraisers, and charity events, not just because they’re still worth an immense amount of money, but because they won. They beat the house.

But does creditor rescue explain too much? If it’s true that bank executives had an incentive to finance risky bets using leverage, why didn’t they take advantage of the implicit guarantee even sooner by investing in riskier assets and using ever more leverage? Banks and investment banks didn’t take wild risks on Internet stocks leading to bankruptcy and destruction. Why didn’t commercial banks and investment banks take on more risk sooner?

One answer is that when the guarantee is implicit, not explicit, creditors can’t finance any investment regardless of how risky it is. If a bank lends money to another bank to buy stock in an Australian gold mining company, it is less likely to get bailed out than if the money goes toward AAA rated assets (which are the highest quality and lowest risk). So some high-risk gambles remain unattractive. That is part of the answer. But the rest of the answer is due to the nature of regulation. In the next section of this paper, I look at why housing and securitized mortgages were so attractive to investors financing risky bets with borrowed money. Bad regulation and an expectation of creditor rescue worked together to destroy the housing market.

6. HOW CREDITOR RESCUE AND HOUSING POLICY COMBINED WITH REGULATION TO BLOW UP THE HOUSING MARKET

The proximate cause of the housing market’s collapse was the same proximate cause of the financial markets’ destruction—too much leverage, too much borrowed money. Just as a highly leveraged investment bank risks insolvency if the value of its assets declines by a small amount, so too does a homeowner.

The buyer of a house who puts 3 percent down and borrows the rest is like the poker player. Being able to buy a house with only 3 percent down, or ideally even less, is a wonderful opportunity for the buyer to make a highly leveraged investment. With little skin in the game, the buyer is willing to take on a lot more risk when buying a house than if he had to put up 20 percent. And for many potential homebuyers, a low down payment is the only way to sit at the table at all.

When prices are rising, buying a house with little or no money down seems like a pretty good deal. Let’s say the house is in California, and the price of the house is $200,000. For $6,000 (3 percent down), the buyer has a stake in an asset that has been appreciating in some markets in some years at 20 percent. If this trend continues, a year from now, the house will be worth $40,000 more than he paid for it. The buyer will have seen a more than six-fold increase in his investment.

What is the downside risk? The downside risk is that housing prices level off or go down. If housing prices do go down a lot, the buyer could lose his $6,000, and he may also lose his house or find himself making monthly payments on an asset that is declining in value and therefore a very bad investment. This is why many homebuyers are currently defaulting on their mortgages and forfeiting any equity they once had in the house. In some states, in the case of default, the lender could go after his other assets as well, but in a lot of states—California and Arizona, for example—the loan is what is called “non-recourse”—the lender can foreclose on the house and get whatever the house is worth but nothing else. Failing to pay the mortgage and losing your house is embarrassing and inconvenient, and, if you have a good credit rating, it will hurt even more. But the appeal of this deal to many buyers is clear, particularly when housing prices have been rising year after year after year.

The opportunity to borrow money with a 3 percent down payment has three effects on the housing market:

It allows people who normally wouldn’t have accumulated a sufficient down payment to buy a house.

It encourages homeowners to bid on larger, more expensive houses rather than cheaper ones.

It encourages prospective buyers to bid more than a house is currently worth if the house is expected to appreciate in value.43

These circumstances all push up the demand for housing. And, of course, if housing prices ever fall, these loans will very quickly be underwater (meaning that the homeowner will owe more on the home than it is currently worth). A small decrease in housing values will cause a homeowner who put 3 percent down to have negative equity much quicker than a buyer who put 20 percent down. With a zero-down loan, the effects are even stronger. But in the early 2000s, a low down payment loan was like a lottery ticket with an unusually good chance of paying off. A zero-down loan was even better. And some loans not only didn’t require a down payment, but also covered closing costs.

Changes in tax policy sweetened the deal. The Taxpayer Relief Act of 1997 made the first $250,000 ($500,000 for married couples) of capital gains from the sale of a primary residence tax exempt.44 Sellers no longer had to roll the profits over into a new purchase of equal or greater value. The act even allowed the capital gains on a second home to be tax-free as long as you lived in that house for two of the previous five years. This tax policy change increased the value of the lottery ticket.c

The cost of the lottery ticket depended on interest rates. In 2001, worried about deflation and recession and the stock market, Alan Greenspan lowered the federal funds rate (the rate at which banks can borrow money from each other) to its lowest level in 40 years and kept it there for about 3 years.45 During this time, the rate on fixed-rate mortgages was falling, but the rate on adjustable-rate mortgages, a short-term interest rate, fell even more, widening the gap between the two. Adjustable-rate mortgages grew in popularity as a result.46

The falling interest rates, particularly on adjustable- rate mortgages, meant that the price of the lottery ticket was falling dramatically. And as housing prices continued to rise, the probability of winning appeared to be going up. (See figure 2.) The upside potential was large. The downside risk was very small—mainly the monthly mortgage payment, which was offset by the advantage of being able to live in the house. Who wouldn’t want to invest in an asset that has a likely tax-free capital gain, that he can enjoy in the meanwhile by living in it, and that he can own without using any of his own money? By 2005, 43 percent of first-time buyers were putting no money down, and 68 percent were putting down less than 10 percent.47

Incredibly, the buyer could even control how much the ticket cost. In a 2006 speech, Fannie Mae CEO Daniel Mudd outlined how monthly loan payments could differ when buying a $425,000 house, the average value of a house in the Washington, DC, area at the time:

With a standard fixed-rate mortgage, the monthly payment is about $2,150.

With a standard adjustable-rate mortgage, the payment drops $65, down to about $2,100 a month.

With an interest-only ARM, the monthly payment drops nearly another $300, down to $1,795.

With an option ARM, the payment could drop another $540, down to roughly $1,250—which in many cases, is less than you’d pay to rent a two-bedroom apartment. Of course, that’s only in the first year.48

In 2005, the average house in the Washington, DC, area grew in value by about 24 percent.49 For the average house bought for $425,000, that’s a gain of more than $100,000. The annual payment of that option adjustable-rate mortgage was $15,000. That’s a pretty cheap lottery ticket for a chance to win $100,000 if prices rise in 2006 by the same amount as the year before. The buyer is paying less than he would in rent, and on top of that, he has a chance to win $100,000. Why wouldn’t a person with limited wealth want to get into that game? Why wouldn’t a person with lots of wealth?

It’s obvious why buyers liked buying houses with little or no money down and the impact that opportunity had on the price of housing, but why would anyone lend money to buyers who had so little money of their own in a transaction? It’s the same question we asked before at the poker table. Why would anyone finance risky bets knowing that the bettor has so little skin in the game?

There are two reasons you might lend a lot of money to someone with no money of his own in the transaction. If home prices are rising and have been for a while, you might be pretty confident that they’ll continue to rise. In that case, the borrower will have equity in the home at the end of the year, and the chance of default will be smaller than it would normally be. You might take a chance and lend the money. But it’s risky.

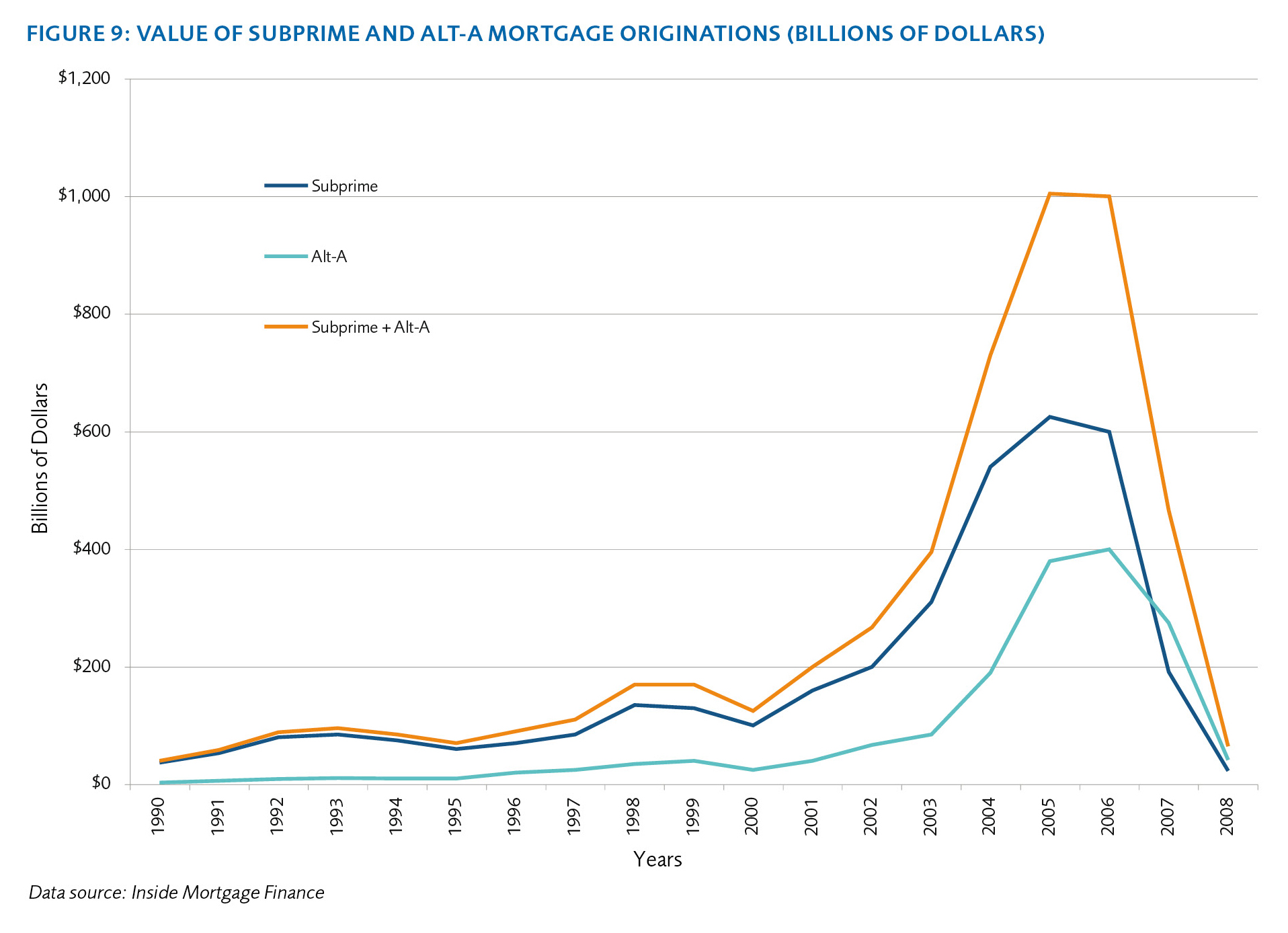

This is one explanation for the explosive growth of mortgage securitization—no one thought housing prices would go down. (See figure 3.) That could be. Yet, historically, nobody made loans where the borrower put little or no money down.

The second reason is that you will be very comfortable lending the money if you know you can sell the loan to someone else. Who is that someone? Between 1998 and 2003, just when the price of houses really started to take off (see figure 2), the most frequent buyers of loans were the GSEs Fannie Mae and Freddie Mac.

Fannie and Freddie bought those loans with borrowed money. Fannie and Freddie were able to borrow the money because lenders were confident that Uncle Sam stood behind Fannie and Freddie.

7. FANNIE AND FREDDIE

The goal of this strategy, to boost homeownership to 67.5 percent by the year 2000, would take us to an all-time high, helping as many as 8 million American families across that threshold. . . . I want to say this one more time, and I want to thank again all the people here from the private sector who have worked with Secretary Cisneros on this: Our homeownership strategy will not cost the taxpayers one extra cent.50

—President Bill Clinton

We want more people owning their own home. It is in our national interest that more people own their own home. After all, if you own your own home, you have a vital stake in the future of our country.51

—President George W. Bush

The federal government’s role in the housing market goes back at least to 1938 with the establishment of the Federal National Mortgage Association (which later became Fannie Mae) and the deductibility of mortgage interest, which is as old as the income tax.52 But the federal government’s role changed fundamentally in the 1990s, when it (along with state governments) pursued a wide array of policies to increase the national homeownership rate. I focus here on the most important change—the expansion of the role of Fannie Mae and Freddie Mac, particularly their expansion into low down payment loans.53

Some argue, Paul Krugman for example, that Fannie and Freddie had nothing to do with the housing crisis. They were not allowed to make low down payment loans; they were not allowed to make subprime loans. They were simply innocent bystanders caught in the crossfire.54 Krugman has also argued a number of times that Fannie and Freddie’s role in housing markets was insignificant between 2004 and 2006: “they pulled back sharply after 2003, just when housing really got crazy.” According to Krugman, Fannie and Freddie “largely faded from the scene during the height of the housing bubble.”

In fact, from 2000 on, Fannie and Freddie bought loans with low FICO scores, loans with very low down payments and loans with little or no documentation—Alt-A loans.55 And between 2004 and 2006, Fannie and Freddie didn’t “fade away” or “pull back sharply.” As I show below, they still bought near-record numbers of mortgages, including an ever-growing number of low down payment mortgages. And while private players bought many more subprime loans than the GSEs, the GSEs purchased hundreds of billions of dollars of subprime mortgage-backed securities (MBS) from private issuers, holding these securities as investments:

Fannie and Freddie bought 25.2% of the record $272.81 billion in subprime MBS sold in the first half of 2006, according to Inside Mortgage Finance Publications, a Bethesda, MD-based publisher that covers the home loan industry.

In 2005, Fannie and Freddie purchased 35.3% of all subprime MBS, the publication estimated. The year before, the two purchased almost 44% of all subprime MBS sold.56

The defenders of Fannie and Freddie are right that Fannie and Freddie’s direct role in subprime lending was smaller than that of purely private financial institutions. But between 1998 and 2003, Fannie and Freddie played an important role in pushing up the demand for housing at the low end of the market. That in turn made subprime loans increasingly attractive to other financial institutions as the prices of houses rose steadily.

7A. It’s Alive!

The word “conduit” is often used to describe Fannie and Freddie’s role in the mortgage market. A conduit is a tube or pipe. Just as a tube or a pipe carries water to raise the level of a reservoir, so Fannie and Freddie added liquidity to the mortgage market, increasing the level of the funds available so that more could partake. That additional liquidity steered by Fannie and Freddie to increase loan availability above and beyond what it would be otherwise seems to be a free lunch of sorts—a way to overcome the natural impediments of timing and risk facing banks and thrifts at very little cost.

Fannie and Freddie increased liquidity to the mortgage market by buying loans from mortgage originators. Banks were happy to sell their loans and give up some of the profit because this meant they wouldn’t have to worry about lending money today that wouldn’t return for years, with all the risks of default, interest rate changes, and prepayment. Fannie and Freddie financed their purchases of loans by issuing debt. They also bundled the mortgages into securities, selling those to investors. Eventually, Fannie and Freddie also used their profits to buy the mortgage-backed securities and collateralized-debt obligations issued by other players in the market.

Fannie and Freddie did indeed make homeownership more affordable and accessible. Joseph Stiglitz, in his book, The Roaring Nineties, argued that the original incarnation of Fannie (as an actual government agency before it was semiprivatized in 1968) was a classic example of fixing a market failure:

Fannie Mae, the Federal National Mortgage Association, was created in 1938 to provide mortgages to average Americans, because private mortgage markets were not doing their job. Fannie Mae has resulted both in lower mortgage rates and higher homeownership—which has broader social consequences. Homeowners are more likely to take better care of their houses and also to be more active in the community in which they live.57

But Fannie and Freddie (created in 1970) were not the textbook creations of economists. At some point, Fannie and Freddie stopped acting like models in a textbook and became something more than conduits. Politicians realized that steering Fannie and Freddie’s activities produced political benefits. And Fannie and Freddie found it profitable to be steered.

Fannie and Freddie had always had certain cost advantages that were not available to purely private players in the mortgage business. They were not subject to the same Securities and Exchange Commission disclosure regulations when they issued mortgage-backed securities. They were not subject to state and local income taxes. Both Fannie and Freddie could tap a credit line of $2.25 billion with the Treasury. The amount of capital they were required to hold was much smaller than that required of private firms.

But the most important advantage for Fannie and Freddie was the implicit government guarantee, embodied in the first letter of their names, the letter F for federal. Fannie Mae’s original name was the Federal National Mortgage Association. Freddie Mac’s was the Federal Home Loan Mortgage Corporation. Investors believed correctly that the federal government stood behind Fannie and Freddie, which were after all called GSEs: government-sponsored enterprises. At the same time, Fannie and Freddie were publicly traded corporations with stockholders.

The business model at Fannie and Freddie was very simple. Because of the government guarantee, they could borrow money cheaply. They could then earn money by buying mortgages that paid a higher rate of interest than the rate Fannie and Freddie had to pay to their lenders. It was a money machine that was incredibly profitable. (See figure 4.) There was only one constraint—the government didn’t let Fannie and Freddie exploit this opportunity fully.

Because the government might be on the hook for any losses, Fannie and Freddie operated under a regulatory regime in which they could buy only what were called “conforming loans”—loans with at least 20 percent down, loans no bigger than a certain amount, and loans with adequate documentation. These restrictions limited Fannie and Freddie’s ability to expand and take advantage of the implicit guarantees from the government. Only so many borrowers can put 20 percent down.

But beginning in 1993, these restraints began to loosen.58 Fannie and Freddie faced new regulations requiring minimum proportions of their loan purchases to be loans made to borrowers with incomes below the median. In 1993, 30 percent of Freddie’s and 34 percent of Fannie’s purchased loans were loans made to individuals with incomes below the median in their area. The new regulations required that number to be at least 40 percent in 1996.59 The requirement rose to 42 percent in 1999 and continued to rise though the 2000s, reaching 55 percent in 2007.60 Fannie and Freddie hit these rising goals every year between 1996 and 2007.61

These requirements seemed like such a good idea at the time. Why not spread the benefits of homeownership more widely? Why not take advantage of the spread between the interest rate at which Fannie and Freddie could borrow and lend? Why not increase Fannie and Freddie’s profits? It seemed like such a magical free lunch: more home owners, more profits, and more politicians who could claim they were helping people.

This brings us to one other group sitting at the table playing with other people’s money: politicians. Politicians are always eager to spend other people’s money. It’s what they do for a living. But it’s an even better deal for politicians if they can hide the fact that they’re spending other people’s money or delay when the bill comes due. That’s what they did with Fannie and Freddie. The politicians told Fannie and Freddie to be a little more flexible with their guidelines. As a result, more people got to own houses and the politicians got to take the credit without having to raise taxes or take away any politically provided goodies from anyone else.

Fannie and Freddie’s increases in loan purchases, especially loans to low-income borrowers, helped inflate the housing bubble. That bubble in turn made the subprime market more attractive and profitable to lenders. It also set the stage for the collapse. Housing policy interacting with the potential for creditor rescue pushed up housing prices artificially. When it all fell apart, the taxpayer paid (and is still paying) the bill.

In the crucial years of housing-price appreciation, between 1997 and 2006 (figure 2), the number of loans bought by Fannie and Freddie expanded dramatically. Figure 5 shows the number of home-purchase loans bought by Fannie and Freddie. Home-purchase loans are loans used by borrowers to purchase homes (rather than to refinance homes). The number jumped by roughly 33 percent in 1998, then by another 25 percent in 2001, and by another 20 percent in 2005. The annual number of loans they purchased doubled between 1997 and 2006.

As figure 6 shows, Fannie and Freddie’s purchases of home-purchase loans made to borrowers with incomes below the median grew even more quickly. These purchases doubled between 1997 and 2003.

Fannie and Freddie’s purchases of low down payment loans (loans with a down payment of 5 percent or less, or a 95 percent loan-to-value ratio) increased at an even faster rate. (See figure 7.)

But if Fannie and Freddie could only buy conforming loans—loans with at least 20 percent down, loans no bigger than a certain amount, and loans with adequate documentation—how did the opportunities available to Fannie and Freddie expand so incredibly? With the encouragement of politicians from both parties, Fannie and Freddie relaxed their underwriting standards, the requirements they placed on originators before they would buy a loan. They called it being more “flexible.”62

For loans made to low-income borrowers, they created special partnerships, using new criteria to determine whether they would buy a loan from an originator.63 They partnered with some of those originators, the traditional lenders—local and national banks—to develop new products with more “flexible” standards and terms.64 And they got fancy with technology.

Around 1995, both Fannie and Freddie unveiled automated software for originating loans: Desktop Underwriter and Loan Prospector, respectively. The software made assessing the riskiness of loans more “scientific” by using credit scores. Fannie and Freddie claimed that based on statistical analyses of the relationship between credit scores and default rates, loans that were once considered too risky were now actually fine.65 These software programs allowed Fannie and Freddie to do an end run around the traditional lenders, creating a cottage industry of mortgage brokers who originated loans for Fannie and Freddie. The software made it cheaper to originate a loan. That was a good thing. But it also allowed more “flexibility” in lending standards, which ended up being a very bad thing.

Christian Science Monitor article from 2000 discusses the impact of automated underwriting:

So for borrowers with good credit, the automated system allows higher debt-to-income ratios than conventional underwriting. That means a borrower might qualify for a larger loan than someone with the same income and poorer credit.

Some other advantages of automated underwriting:

*It requires less documentation. “Where three months of bank statements and pay-check stubs are required for conventional underwriting, only one month is typically required by the automated system,” says Ms. James.

*Borrowers are being approved for loans that they would have been turned down for just a year or two ago.

“By analyzing the credit assessments done by Desktop Underwriter, we found that lower-income families have credit histories that are just as strong as wealthier families,” said Fannie Mae chief executive Frank Raines in a speech to the National Association of Home Builders. As a result, 44 percent of Fannie Mae’s business is now conducted with low- and moderate-income families. Mr. Raines added that having a strong credit history could offset the need for a large down payment.66

The most important change at Fannie and Freddie, however, was their approach to the down payment. In 1997, fewer than 3 percent of Fannie and Freddie’s loans had a down payment of less than 5 percent.67 But starting in 1998, Fannie created explicit programs where the required down payment was only 3 percent. In 2001, it even began purchasing loans with zero down. With loans that had a down payment, it stopped requiring the borrower to come up with the down payment out of his own funds. Down payments could be gifts from friends or, better still, grants from a nonprofit or government agency.

These changes weren’t secret; executives and politicians bragged about how Fannie and Freddie were buying riskier loans. Frank Raines, the CEO of Fannie Mae at the time, testified before the U.S. House Committee on Financial Services in 2002:

For example, a down payment is often the single largest obstacle preventing a family from purchasing a home. Fannie Mae was at the forefront of the mortgage industry expansion into low-down payment lending and created the first standardized 3-percent-down mortgage. Fannie Mae financing for low down payment loans (5 percent or less) has grown from $109 million in 1993 to $17 billion in 2002.

We’ve also used technology to expand our underwriting criteria, so that we can reach underserved communities. For example, our Expanded Approval products make it possible for people with blemished credit to obtain a conforming mortgage loan. And we’ve added a Timely Payments Reward feature to those loans, enabling borrowers to lower their mortgage payment by making their payments on time. These mortgage features have been crucial tools in reaching into communities that were previously underserved. The mortgage market today has a wider variety of products available than ever before, and therefore is better poised to meet the individual financing needs of a broader range of homebuyers.68

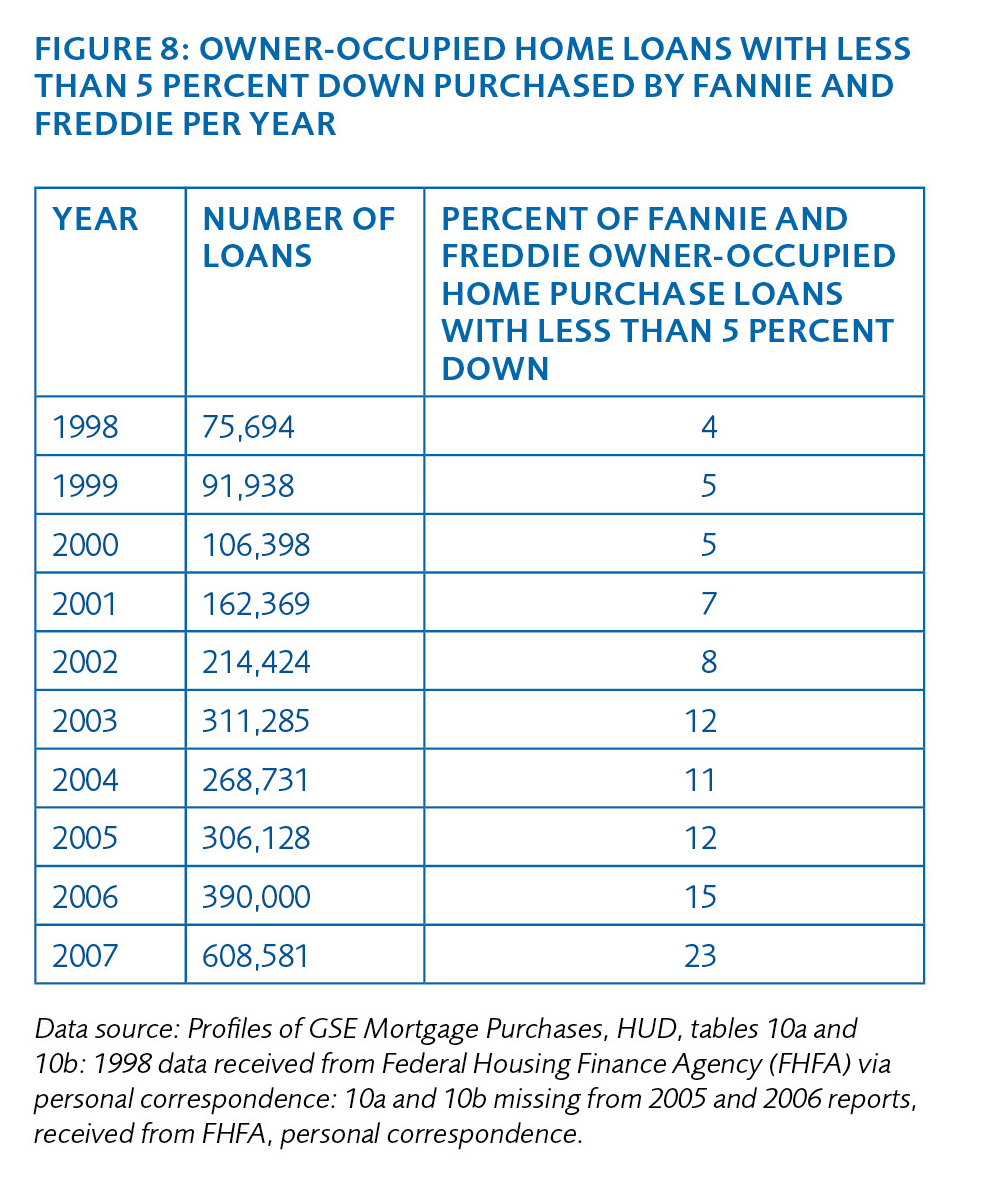

Between 1998 and 2003, the absolute number of loans purchased by Fannie and Freddie with less than 5 percent down more than quadrupled. (See figure 8.) Also by 2003, 714,000 loans—28 percent of Fannie and Freddie’s total volume of home purchase loans—were loans with less than 10 percent down.69

When the down payment was less than 20 percent, Fannie and Freddie required private mortgage insurance (PMI). On a zero down payment loan, for example, the borrower would take out insurance to cover 20 percent of the value of the loan, protecting Fannie and Freddie from the risk of the borrower defaulting. But starting in the 1990s, an alternative to PMI emerged—the piggyback loan, a second loan that finances part or all of the down payment. The use of piggyback loans grew quickly beginning in the 1990s through 2003 and even more dramatically in the 2004–2006 period.70 For example, in a study of the Massachusetts mortgage market, the Warren Group found that in 1995, piggyback loans were 5 percent of prime mortgages. The number grew to 15 percent by 2003. By 2006, over 30 percent of prime mortgages in Massachusetts were financed with piggyback loans. For subprime loans in Massachusetts, almost 30 percent were financed with piggybacks in 2003 and more than 60 percent by 2006.71

There are no public data yet available on how many of Fannie’s loans with 20 percent down were really piggyback loans with zero down—loans where the borrower had no equity in the house. Suffice it to say that Fannie and Freddie contributed to the zero or low down payment frenzy with their support of 3 percent down and eventually no money down loans. The full extent of Fannie and Freddie involvement in low down payment loans is unclear because of the piggyback phenomenon. Maybe we’ll find out down the road.

7B. What Steering the Conduit Really Did

Whether one measures by the total number of loans or by dollar volume, Fannie and Freddie took the originate-and-sell model of mortgage lending through the roof. What was really going on? Individuals, institutions, and governments were lending money to Fannie and Freddie, who used that money to buy loans from originators, who gave that money to people, who used that money to buy homes. Fannie and Freddie were conduits for investors to make loans to homeowners. Fannie and Freddie did so in wildly increasing amounts even as the quality of the loans deteriorated. Perhaps they did it in blind exuberance. But they were encouraged to be blind. When the government implicitly backed Fannie and Freddie, it severed the usual feedback loops of a market system.

The fees that Fannie and Freddie paid their originators made origination extremely profitable. Because there was no feedback loop that punished bad loans, many more bad loans were made. Not only did people borrow money as a lottery ticket, but surely originators encouraged potential homeowners by deceiving them about the financial products they were buying.72 The implicit guarantee of Fannie and Freddie and the housing mandates removed the normal restraints of prudence on homeowners and originators.

Consider an investing odd couple: the Chinese government on the one hand and my father, a cautious investor in his 70s, on the other. Both invested in Fannie and Freddie bonds because they paid more interest than Treasuries and were probably just as safe. They weren’t paying attention to what was going on with Fannie and Freddie’s portfolio of loans because they didn’t need to. They counted on the implicit guarantee. It was a free lunch for my father and the Chinese—a good return without any risk. We know investors weren’t paying attention because between 2000 and 2006, even as Fannie and Freddie took on more and more risk, Fannie and Freddie’s borrowing costs stayed constant or even fell relative to Treasuries. The market viewed bonds issued by Fannie and Freddie as almost interchangeable with Treasuries. Alas, the market was right.73

The American taxpayer ultimately paid for that “free lunch.” And a few trillion dollars flowed from the Chinese and my father and other investors into new houses and bigger houses because the Fannie and Freddie conduit offered such an attractive mix of risk and reward. That flow of money was terribly costly: channeling precious capital into housing meant it didn’t flow into other areas that were more valuable but that were artificially made less attractive. So we got more and bigger houses and less of something else—less money going to fund new medical devices, cars that get better gas mileage, more creative entertainment, or something else creative people could have done with more capital.

8. FANNIE AND FREDDIE—CAUSE OR EFFECT?

People inside the mortgage and investment world have two different perspectives on Fannie and Freddie’s role. The first view is that Fannie and Freddie were followers, not leaders. They put up with the affordable-housing mandates because they were already involved in loans to low-income borrowers. They loosened credit standards between 1998 and 2003 to keep market share. They got involved in Alt-A and subprime loans in 2005 and 2006 for the same reason. They were just victims of the crisis.74